How to Buy Repo Cars Directly From Banks (Without Dealer Fees)

Most people think the only way to buy a car is from a dealership. But there is another way that many buyers never discover.

Banks and credit unions regularly repossess vehicles when borrowers stop making payments. Instead of keeping these vehicles, financial institutions usually sell them quickly to recover their loan balance.

The surprising part is that many of these repossessed vehicles are available directly to the public. When you buy repo cars directly from banks, you often avoid dealer markups, auction fees, and unnecessary middlemen.

That is where the real savings can happen.

In this guide, you will learn how to buy repo cars directly from banks, where to find them, and how to avoid the mistakes many buyers make.

Why Banks Sell Repossessed Vehicles

Banks do not want to be in the car business.

When a borrower defaults on an auto loan, the lender repossesses the vehicle to recover the remaining balance of the loan. Their goal is simple: sell the car as quickly as possible and recover their money.

Because of this, banks are often motivated sellers.

They usually price repossessed vehicles below normal retail value so they can move inventory quickly.

Unlike dealerships, banks are not trying to maximize profit on each vehicle. They are trying to close out a loan.

This creates an opportunity for buyers who know where to look.

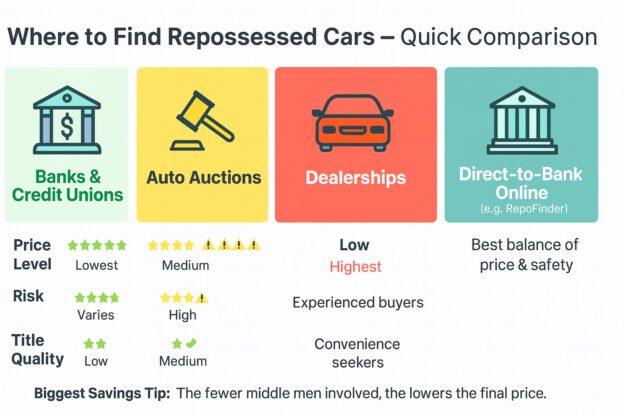

The Problem With Repo Auctions

Many websites claim the best way to buy repossessed cars is through auctions.

But auctions are not ideal for most buyers.

Here are some common issues:

1. Dealer competition

Professional car dealers attend auctions regularly and often outbid private buyers.

2. Auction fees

Many auctions charge buyer fees that can add hundreds or even thousands of dollars to the final price.

3. Limited inspection

Auction vehicles are often sold as-is with little time for inspection.

4. Dealer-only auctions

Many of the best repo auctions are restricted to licensed dealers.

Because of these challenges, auctions can be difficult for everyday buyers.

The Better Way: Buy Repo Cars Directly From Banks

A better option is to buy repossessed vehicles directly from banks and credit unions.

Many financial institutions list their repossessed vehicles on their own websites or through specialized directories.

When you buy directly from the lender, you avoid many of the costs and complications associated with auctions.

Benefits often include:

• No dealer markup

• No auction competition

• Transparent pricing

• Access to financing from the same bank

Many buyers do not realize this option exists, which is why it can be such a valuable opportunity.

Where to Find Bank Repo Cars

The hardest part of buying repossessed vehicles is simply finding them.

Thousands of banks and credit unions across the United States repossess vehicles every year, but their listings are scattered across hundreds of different websites.

This is where a directory like RepoFinder.com becomes extremely useful.

Instead of searching bank websites one by one, RepoFinder organizes repossessed vehicle listings from banks and credit unions across the country in one place.

You can browse repos from:

• Local banks

• Credit unions

• Regional lenders

• National financial institutions

This allows buyers to quickly locate repossessed vehicles that are actually being sold by the lender.

You can start searching here:

Types of Repo Vehicles You Can Find

Many people assume repossessions only include cheap or heavily used vehicles. That is not true.

Banks repossess vehicles of all types.

Common repo listings include:

• Cars

• Trucks

• SUVs

• RVs

• Boats

• Motorcycles

• ATVs

Sometimes repossessions include nearly new vehicles with relatively low mileage.

In many cases, the previous owner simply experienced financial hardship rather than neglecting the vehicle.

Steps to Buying a Repo Car From a Bank

Buying a repossessed vehicle is usually straightforward.

Here is the typical process.

Step 1: Find available repossessions

Use a directory like RepoFinder to locate repossessed vehicles from banks and credit unions.

Step 2: Contact the lender

Once you find a vehicle you are interested in, contact the bank or credit union directly.

They can provide details about the vehicle and the purchase process.

Step 3: Inspect the vehicle

If possible, inspect the vehicle in person or have a mechanic check it.

Most repos are sold as-is, so doing your homework is important.

Step 4: Make an offer or purchase

Some lenders accept offers, while others list a fixed price.

If your offer is accepted, you can complete the purchase directly with the bank.

Can You Finance a Repo Car?

Yes.

In fact, many banks prefer to finance repo vehicles themselves.

If you have decent credit, the lender may offer financing options for the vehicle they are selling.

This can make the purchase process even easier.

Are Repo Cars a Good Deal?

Often, yes.

Because banks are motivated to sell quickly, repo vehicles can sometimes be priced below market value.

However, buyers should always research the vehicle and compare prices before purchasing.

Like any used car purchase, doing proper due diligence is important.

Final Thoughts

Buying repossessed vehicles directly from banks is one of the most overlooked ways to save money on a car purchase.

Instead of competing with dealers at auctions or paying dealership markups, buyers can sometimes purchase vehicles straight from the lender.

The key is simply knowing where to look.

Directories like RepoFinder.com make it much easier to locate bank-owned vehicles and connect buyers directly with financial institutions selling repossessions.

If you are searching for a vehicle and want to explore repo listings from banks and credit unions, it is a great place to start.