Are Bank Car Auctions Legit? A Safe Buyer’s Guide to Bank Repossessed Cars

TL;DR

Yes, real bank car auctions are legitimate. Banks sell repossessed vehicles to recover unpaid loans, not to make retail profit. Most bank repos have clean titles and sell below dealer prices. The risk comes from fake auction sites and dealer middlemen pretending to be banks. If you verify ownership, title status, and VIN, buying a car directly from a bank can be one of the safest and cheapest ways to buy a used vehicle.

If you’ve searched for cheap cars online, you’ve probably seen the phrase “bank car auctions.”

And if you’re like most people, your next thought was:

“Is this legit, or is this another scam?”

That’s a fair question.

The used car world is full of confusing terms, misleading listings, and websites that look official but are not.

So let’s slow this down and explain how bank car auctions actually work, what’s real, what’s not, and how regular people buy repossessed cars directly from banks without getting burned.

What Is a Bank Car Auction?

A bank car auction is when a bank or credit union sells a vehicle it repossessed after a loan default.

Banks are not car dealers.

They do not want inventory.

They want their money back.

Instead of fixing the car up and reselling it like a dealer would, banks usually sell repossessed vehicles as is, often at wholesale level pricing.

That is where the opportunity comes from.

Are Bank Car Auctions Legit?

Yes. Real bank car auctions are legitimate.

Here is the important part.

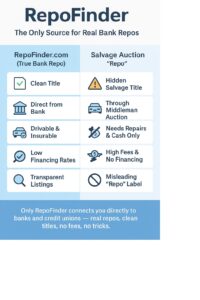

Not every website that claims to sell bank repos is actually connected to a bank.

That distinction matters.

Why People Think Bank Auctions Are Sketchy

Most horror stories come from one of these situations:

• Fake “auction” websites charging access fees

• Salvage or insurance auctions mislabeled as bank repos

• Dealer middlemen pretending to be banks

• Cars with hidden title problems

When people say bank auctions are risky, they are usually talking about the wrong kind of auction.

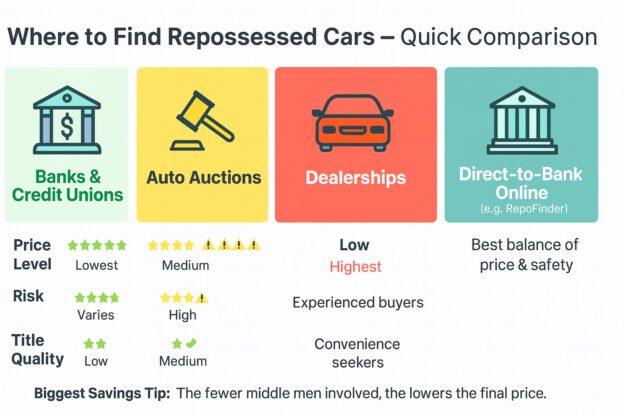

Bank Repos vs Dealer and Salvage Auctions

Here is a simple breakdown.

Bank Repossessed Cars

• Owned by banks or credit unions

• Usually have clean titles

• Regular used vehicles

• Not insurance write offs

• Sold to recover loan balances

Salvage or Insurance Auctions

• Totaled or heavily damaged vehicles

• Salvage or rebuilt titles

• Often flood, collision, or theft losses

• Higher risk

• Not bank owned

If a listing does not clearly say who owns the vehicle, that is a red flag.

Do Bank Repo Cars Have Clean Titles?

Most do.

Banks financed these vehicles originally.

That means the car was road legal when the loan started.

Repossession does not damage a title.

There are exceptions:

• Abandoned vehicles

• Rare legal complications

• Extreme neglect

That is why buyers should always:

• Ask about the title

• Run a VIN report

• Confirm ownership before buying

Can Anyone Buy From a Bank Car Auction?

Yes. In many cases, anyone can buy.

You usually do not need:

• A dealer license

• Auction credentials

• Special access

Some banks sell directly.

Others list vehicles online.

Some work through local branches.

The challenge is finding them.

Banks do not advertise repossessed cars aggressively.

They do not optimize listings for search engines.

And they do not want tire kickers.

Why Banks Sell Repossessed Cars Cheap

Banks are not trying to maximize profit.

They want to:

• Close the loan

• Remove liability

• Clear the asset from their books

Holding vehicles costs money.

Every extra week hurts them.

That is why bank repos often sell below dealer pricing, even when the car runs and drives.

How to Tell If a Bank Car Auction Is Legit

Use this checklist:

• The seller is clearly identified as a bank or credit union

• No membership or access fees

• VIN is provided

• Title status is disclosed

• No pressure tactics

• No vague phrases like “bank style pricing”

If ownership details are hidden, walk away.

Step by Step: How to Buy a Car Directly From a Bank

-

Find the listing

Look for repossessed vehicles owned by banks or credit unions, not dealers pretending to be banks. -

Research the vehicle

Run a VIN check.

Compare market value.

Look for obvious red flags. -

Ask smart questions

Title status

Location

Payment method

Inspection options -

Inspect if possible

Some banks allow inspections.

Some do not.

Factor this into your offer. -

Make an offer or bid

Many bank sales are simple best offer transactions, not bidding wars. -

Pay and transfer title

Banks move slower but follow formal processes.

Expect paperwork, not surprises.

Common Myths About Bank Car Auctions

1- Myth: Only dealers get the good cars

1- Truth: Dealers just know where to look

2-Myth: All bank repos are trashed

2-Truth: Many were repossessed due to missed payments, not abuse

3-Myth: You will get scammed

3-Truth: Scams happen when ownership is not verified

Why Buying Direct Beats Buying From Dealers

Dealers:

• Add markup

• Add fees

• Recondition cheaply

• Control the narrative

Banks:

• Sell as is

• Disclose ownership

• Do not upsell

• Do not play games

Different incentives lead to different outcomes.

FAQs

Are bank car auctions safe?

Yes, when the vehicle is truly bank owned and the title is verified.

Are bank repos cheaper than dealers?

Often yes, because banks are not selling for retail profit.

Do bank repos have clean titles?

Most do, since they were financed as standard vehicles.

Can I buy a bank repo online?

Yes. Many banks now sell repossessed vehicles digitally.

Final Takeaway

Bank car auctions are not shady.

Shady websites are.

When you understand how repos work, who owns the vehicle, and how banks operate, buying a repossessed car can be one of the smartest ways to avoid dealer games and overpaying.

Access matters more than luck.