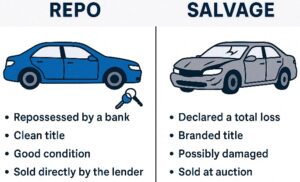

Not All “Repos” Are the Same – The Truth About Bank Repos vs. Salvage “Repos”

Most shoppers see the word repo and think it means a great deal. But here’s the truth: not all repos are the same.

Some “repo” listings are real, clean title vehicles owned and sold directly by banks or credit unions.

Others use the word “repo” as clickbait to hide wrecked or totaled vehicles coming from insurance pools or salvage auctions.

If you’re shopping for a used car, understanding the difference could save you thousands, and protect you from a bad surprise at registration time.

Let’s break it down.

1. The Source: Real Bank Repos vs. Salvage Yard “Repos”

Every car has a story, and where it comes from tells you everything about its condition.

True bank repos, like the ones listed on RepoFinder.com, come straight from the lender who financed them.

When a borrower stops making payments, the bank reclaims the car. They don’t want to own cars, they just need to recover the loan balance.

So, they sell the repossessed vehicle directly to the public. Simple. Honest. Transparent.

Salvage seller “repos” are totally different. These cars weren’t repossessed because of missed payments, they were totaled by insurance companies. After an accident, flood, or theft claim, the vehicle is marked as a total loss. Then, insurance auctions or third-party resellers list those cars online, often calling them “repos” to attract clicks.

That single word swap confuses thousands of buyers every year.

2. The Title Status: Clean Titles vs. “Clean Until Registered”

Here’s where most people get burned.

When you buy from a bank or credit union through RepoFinder, you’re usually getting a clean title.

That means the car has never been totaled, rebuilt, or branded. When you register it, it stays clean.

Banks rarely deal with damaged or flood vehicles. They just want to move unpaid inventory.

But many salvage sellers show listings with “clean” titles that aren’t really clean at all.

Why? Because the DMV hasn’t updated the paperwork yet.

Once you try to register that “clean title” car, the truth comes out, it’s suddenly branded salvage or rebuilt.

By then, it’s too late. The value drops by 30–50%, and you’re stuck with a car that’s difficult to finance or insure.

What looked like a deal quickly turns into a headache.

3. The Condition: Road-Ready vs. Repair Projects

When you browse bank repos on RepoFinder, you’ll notice something right away, most look like normal used cars.

That’s because they are normal used cars. They were everyday drivers before being repossessed for missed payments.

They may need a basic cleaning or a few small repairs, but they’re usually drivable and safe.

Now, compare that to salvage repos. Many of those vehicles are wrecked, stripped, flooded, or burned. Some are missing major parts. Others don’t run at all.

You’re not buying transportation, you’re buying a rebuild project.

And unless you’re a body shop or a professional rebuilder, those “cheap” cars can end up costing more than a clean repo from a bank.

4. The Buying Process: Direct to Bank vs. Fee-Filled Auctions

Buying a real repo is straightforward.

On RepoFinder, you connect directly with banks and credit unions that sell repos to the public.

There’s no middleman, no dealer markup, and no hidden fees.

You contact the lender, arrange a viewing, and make an offer.

Compare that to buying from a salvage auction.

You’ll often pay “buyer’s premiums,” “gate fees,” “document fees,” and “storage fees.”

Some sites even require a dealer license or paid membership just to bid.

And once you win, you still have to arrange towing, repair, and re-inspection before it’s street legal.

RepoFinder’s process feels more like buying from a private party, but safer, because banks handle the title transfer and bill of sale professionally and at no cost.

5. Financing and Insurance: Easy Approval vs. Roadblocks

Here’s another big difference that buyers overlook.

When you buy a clean title repo from a bank, that same bank may offer special repo financing.

These programs are designed to move vehicles quickly, with interest rates as low as 1–3%.

You could save hundreds a month compared to dealer financing.

Clean title vehicles are also easy to insure. You can get full coverage just like any other used car.

But salvage “repos”?

Most lenders won’t touch them, they’re cash only.

Even if you pay cash, insurance companies often refuse full coverage. You’ll get liability only, which leaves you unprotected if the car is damaged again.

A clean title repo doesn’t just save money upfront, it saves you stress for years down the road.

6. Long-Term Value: An Asset vs. a Liability

A clean title repo is still a real asset.

You can sell it later, trade it in, or refinance it.

It keeps its value because it’s legally recognized as a standard used vehicle.

A salvage vehicle, on the other hand, is a permanent liability.

Once a title is branded salvage or rebuilt, it can never go back to clean.

Even if you spend thousands restoring it, its resale value stays low. Dealers rarely accept them as trade-ins, and many buyers won’t touch them.

That’s the long-term price of buying the wrong kind of “repo.”

7. Transparency and Trust: RepoFinder vs. the Rest

RepoFinder doesn’t sell cars. It simply connects buyers to verified banks and credit unions across all 50 states.

You browse listings by state, click a lender, and contact them directly.

No games. No third-party middlemen pretending to be banks.

Each listing represents a real financial institution trying to clear real repos from its books.

You deal with the lender directly, not an auction house or a reseller hiding behind the word “repo.”

That’s why buyers trust RepoFinder, it’s transparent, simple, and completely free to use.

8. Why Salvage Sellers Misuse the Word “Repo”

It’s all about marketing.

The word repo sounds safer and cleaner than salvage.

When people hear “repo,” they think “someone couldn’t make payments,” not “someone crashed this into a ditch.”

So salvage sellers borrow the term to make their listings sound more appealing.

But they’re counting on buyers not knowing the difference.

They blur the line between financial repossession and physical damage to attract traffic.

RepoFinder draws that line clearly.

A real repo means it came from a financial institution, not a salvage yard.

9. Common Myths About Repos and Salvage Cars

#1 Myth: “A repo car is probably trashed.”

➡️ Truth: Most repos are in good shape, they were parked at home, not wrecked.

#2 Myth: “A salvage car with a clean title is still a good deal.”

➡️ Truth: It may look clean online, but registration reveals the truth.

#3 Myth: “Banks don’t sell directly to the public.”

➡️ Truth: Thousands do, and RepoFinder lists them all in one place.

#4 Myth: “Auction sites are cheaper.”

➡️ Truth: Add up the hidden fees, repairs, and title issues, and bank repos almost always win.

10. The Smart Shopper’s Advantage

When you buy a real repo from a bank or credit union, you’re stepping into a transaction built on fairness.

There’s no upsell, no pressure, and no hidden agenda.

Banks want their money back, not a commission. That’s why prices are often lower than dealer lots, sometimes far lower.

Salvage sellers, on the other hand, profit from damaged inventory. Their goal isn’t to help you drive, it’s to move junk fast.

If you’re a regular buyer looking for dependable transportation, RepoFinder gives you a smarter, safer way to shop.

It’s the only platform that keeps “repo” honest.

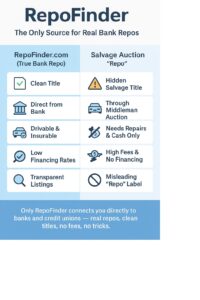

11. Quick Comparison: Bank Repo vs. Salvage Seller “Repo”

| Feature | Bank Repo (RepoFinder.com) | Salvage Seller “Repo” |

|---|---|---|

| Source | Bank or Credit Union | Insurance Auction / Tow Yard |

| Title | Clean and Transferable | Clean Until Registration → Salvage |

| Condition | Drivable, Well-Maintained | Wrecked or Flooded |

| Fees | None | Multiple Hidden Fees |

| Financing | Often Available | Usually Cash Only |

| Insurance | Full Coverage OK | Limited or Liability Only |

| Resale Value | Strong | Permanently Reduced |

| Transparency | Direct-to-Lender | Middleman or Auction |

| Best Site | RepoFinder.com | Misleading “Repo” Auctions |

12. The Bottom Line

A real repo is a financial event, not a physical wreck.

Banks and credit unions repossess vehicles for missed payments, not because of damage.

Salvage sellers misuse the word “repo” to attract attention. They count on confusion to move totaled vehicles.

But now you know the truth.

If you want a real clean title deal, with no middlemen, no fees, and no surprises, go straight to the source.

👉 Visit RepoFinder.com.

It’s the nation’s largest free directory of banks and credit unions selling repos directly to the public.

Real repos. Clean titles. Honest deals.