TL;DR: Repo motorcycles commonly range from about $2,000 for older beginner bikes and dirt bikes to more than $25,000 for newer touring motorcycles and trikes. Prices depend on the motorcycle’s age, mileage, brand, condition, location, and demand. A repo bike may cost less than similar dealer inventory, but buyers should also account for repairs, transportation, taxes, registration, and seller fees.

Browse current repo motorcycles for sale

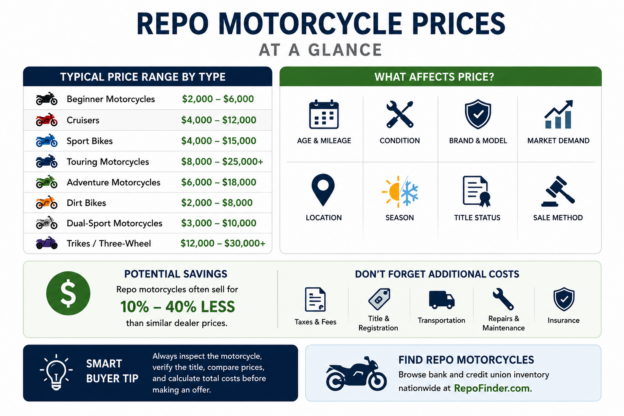

How much do repo motorcycles cost? The answer depends on the type of motorcycle, its condition, mileage, model year, location, and current market demand. Some older repossessed motorcycles sell for only a few thousand dollars, while newer touring bikes and three-wheel motorcycles can cost more than $25,000.

Banks and credit unions often sell repossessed motorcycles after recovering them from borrowers who stopped making loan payments. Because financial institutions usually want to recover their money and reduce storage expenses, buyers may find competitive prices. However, a repossessed motorcycle is not automatically a bargain.

This guide explains typical repo motorcycle prices, the factors that affect value, and how to determine whether a lender-owned motorcycle offers a good deal.

What Is a Repo Motorcycle?

A repo motorcycle is a motorcycle that a bank, credit union, or other lender recovered after the borrower failed to meet the terms of a loan agreement.

After repossession, the lender usually sells the motorcycle to recover part of the unpaid loan balance. The financial institution may advertise the bike directly, accept offers, request sealed bids, or use a third-party auction company.

Repossession describes the motorcycle’s financing history. It does not necessarily mean the motorcycle has accident damage or a salvage title. A well-maintained motorcycle can become a repossession because its owner experienced financial hardship.

Average Repo Motorcycle Prices by Type

Repo motorcycle prices vary widely. Still, the following estimates provide a general starting point for shoppers.

| Motorcycle Type |

Typical Repo Price Range |

| Beginner motorcycles |

$2,000 to $6,000 |

| Cruisers |

$4,000 to $12,000 |

| Sport bikes |

$4,000 to $15,000 |

| Touring motorcycles |

$8,000 to $25,000+ |

| Adventure motorcycles |

$6,000 to $18,000 |

| Dirt bikes |

$2,000 to $8,000 |

| Dual-sport motorcycles |

$3,000 to $10,000 |

| Trikes and three-wheel motorcycles |

$12,000 to $30,000+ |

These ranges are estimates rather than guaranteed selling prices. A newer motorcycle with low mileage may sell above the listed range, while a damaged or non-running bike may sell for less.

Repo Motorcycle Prices by Popular Brand

Brand reputation, reliability, parts availability, and buyer demand can significantly affect resale value.

Harley-Davidson Repo Motorcycle Prices

Harley-Davidson motorcycles often retain value because of strong brand recognition and demand for cruisers and touring models.

- Sportster: approximately $4,000 to $8,000

- Softail: approximately $7,000 to $15,000

- Street Glide: approximately $10,000 to $22,000

- Road Glide: approximately $12,000 to $25,000

- Harley-Davidson trikes: approximately $15,000 to $30,000+

Custom accessories may increase buyer interest, but they do not always add their full purchase cost to the motorcycle’s resale value.

Honda Repo Motorcycle Prices

Honda motorcycles are popular because of their reliability, broad model selection, and widely available replacement parts.

- Honda Rebel: approximately $3,000 to $6,000

- Honda CB500 series: approximately $4,000 to $7,000

- Honda Shadow: approximately $3,500 to $8,000

- Honda Africa Twin: approximately $8,000 to $15,000

- Honda Gold Wing: approximately $10,000 to $22,000+

Yamaha Repo Motorcycle Prices

Yamaha offers commuter motorcycles, cruisers, sport bikes, adventure motorcycles, and off-road models.

- Yamaha MT-03: approximately $3,500 to $5,500

- Yamaha MT-07: approximately $5,500 to $8,500

- Yamaha YZF-R models: approximately $5,000 to $15,000

- Yamaha Tenere 700: approximately $8,000 to $12,000

- Yamaha Star cruisers: approximately $4,000 to $12,000

Kawasaki Repo Motorcycle Prices

Kawasaki listings often include Ninja sport bikes, Vulcan cruisers, Versys touring models, and KLR dual-sport motorcycles.

- Kawasaki Ninja 400: approximately $3,500 to $6,000

- Kawasaki Ninja ZX models: approximately $6,000 to $16,000

- Kawasaki Vulcan: approximately $4,000 to $11,000

- Kawasaki Versys: approximately $5,000 to $12,000

- Kawasaki KLR650: approximately $4,000 to $8,000

Other Repo Motorcycle Brands

Banks and credit unions may also sell motorcycles from:

- Suzuki

- Indian

- BMW

- Ducati

- KTM

- Triumph

- Can-Am

- Aprilia

- Moto Guzzi

- Victory

Premium and specialty brands may command higher prices. However, they can also cost more to repair and maintain.

What Affects the Price of a Repo Motorcycle?

Several factors determine how much a lender asks for a repossessed motorcycle.

Model Year

Newer motorcycles usually cost more because they may include updated technology, lower mileage, modern safety features, and stronger market demand.

Older motorcycles often cost less, although rare or collectible models may not follow normal depreciation patterns.

Mileage

Lower mileage can increase a motorcycle’s value. However, mileage does not tell the entire story. A well-maintained motorcycle with moderate mileage may offer better value than a low-mileage bike that sat unused outdoors.

Mechanical Condition

Mechanical condition has a major effect on price. A motorcycle that starts, runs, shifts, and stops properly will usually attract more buyers than a non-running motorcycle.

Potential repair items include:

- Tires

- Brakes

- Battery

- Chain and sprockets

- Drive belt

- Fork seals

- Fuel system

- Cooling system

- Electrical components

- Engine or transmission repairs

Cosmetic Condition

Scratches, dents, cracked fairings, faded paint, torn seats, and corrosion can reduce value. Cosmetic damage may not affect safety, but it can reveal how the previous owner stored or handled the motorcycle.

Title Status

A motorcycle with a standard title usually sells for more than a comparable motorcycle with a salvage, rebuilt, flood, or junk title.

Always verify the title status before making an offer. Repossession alone does not automatically create a branded title.

Location

Prices and demand can vary by region. Cruisers may sell differently in one state than adventure motorcycles, dirt bikes, or sport bikes.

Transportation costs also matter. A motorcycle priced below market value may become less attractive if it requires expensive cross-country shipping.

Season and Weather

Motorcycle demand often increases during spring and early summer. In colder climates, demand may slow during late fall and winter.

However, seasonal pricing depends on local weather, inventory, seller motivation, and the type of motorcycle. Buyers should not assume that one month always produces the lowest prices.

Sale Method

The lender may use a fixed price, negotiated sale, sealed bid, or public auction. Each method can produce different results.

A fixed-price listing gives buyers a clear starting point. An auction may begin with a low bid, but competition and buyer fees can increase the final cost.

Are Repo Motorcycles Cheaper Than Dealership Motorcycles?

Repo motorcycles can cost less than comparable dealer inventory, but not every lender-owned bike carries a large discount.

Dealership pricing may include:

- Inspection and reconditioning

- Showroom expenses

- Sales commissions

- Advertising costs

- Warranty coverage

- Dealer profit

Banks and credit unions have different priorities. They generally want to recover the loan balance and remove the motorcycle from inventory. As a result, some lenders may accept competitive offers.

However, dealerships may provide benefits that lenders do not, including service records, reconditioning, test rides, financing options, and limited warranties. Buyers should compare the entire transaction rather than the advertised price alone.

For a detailed comparison, read Buying a Motorcycle: Dealer vs. Private Party vs. Bank Repo.

How Much Can You Save on a Repo Motorcycle?

There is no universal discount for repossessed motorcycles. Savings depend on the lender’s asking price, the motorcycle’s market value, its condition, and the number of interested buyers.

For example, consider a motorcycle with a typical retail value of $8,000:

- Lender asking price: $6,800

- Transportation: $400

- New battery: $150

- Tire replacement: $500

- Registration and taxes: varies by state

The motorcycle appears to offer a $1,200 discount before additional expenses. After transportation and repairs, the real savings may be much smaller.

Therefore, calculate the motorcycle’s total cost before deciding whether it represents a good deal.

Cheapest Types of Repo Motorcycles

Buyers searching for affordable motorcycles may find good values among smaller, older, or less complicated models.

Common budget-friendly options include:

- Honda Rebel

- Honda Shadow

- Kawasaki Ninja 300 or Ninja 400

- Kawasaki Vulcan

- Yamaha MT-03

- Yamaha V Star

- Suzuki SV650

- Suzuki Boulevard

- Older Harley-Davidson Sportsters

- Small dual-sport motorcycles

- Older dirt bikes

These motorcycles often have lower purchase prices and widely available replacement parts. Insurance and maintenance may also cost less than they do for high-performance or luxury touring motorcycles.

When Is a Cheap Repo Motorcycle a Bad Deal?

A low asking price does not guarantee a good value. The motorcycle may require repairs or documentation that significantly increases the final cost.

Watch for:

- Missing keys

- Dead or damaged batteries

- Old or cracked tires

- Fuel-system problems caused by long-term storage

- Frame or accident damage

- Engine or transmission noises

- Electrical problems

- Missing title paperwork

- Unexpected auction or buyer fees

- High transportation costs

A motorcycle priced $2,000 below market value may not save money if it needs $3,000 in repairs.

Calculate the Total Cost Before You Buy

Use the following formula when comparing a repo motorcycle with dealer or private-party listings:

Total purchase cost = motorcycle price + seller fees + taxes + registration + transportation + immediate repairs

Also consider future ownership expenses such as insurance, routine maintenance, replacement parts, riding gear, and storage.

How to Determine a Fair Price

Before making an offer, compare the repo motorcycle with similar motorcycles for sale in your area.

Compare Similar Motorcycles

Look for motorcycles with the same:

- Year

- Make

- Model

- Trim

- Mileage range

- Title status

- Condition

A dealer’s retail price may be higher than private-party value. Therefore, compare several sources instead of relying on a single listing.

Estimate Immediate Repairs

List every known repair and estimate the cost of parts and labor. If the motorcycle needs professional inspection, towing, or shipping, include those expenses as well.

Set a Maximum Offer

Determine your maximum price before bidding or negotiating. This step reduces the chance that excitement or auction competition will push you beyond the motorcycle’s actual value.

Can You Negotiate the Price of a Repo Motorcycle?

Some lenders accept offers below the listed price, while others use firm pricing or sealed bids. The seller’s willingness to negotiate may depend on how long the motorcycle has been listed and how much interest it has received.

Support your offer with facts such as:

- Comparable motorcycle prices

- Visible damage

- Required repairs

- Missing keys or documentation

- Transportation expenses

A realistic offer based on the motorcycle’s condition is more likely to receive consideration than an unsupported low offer.

Do Banks Finance Repo Motorcycles?

Some banks and credit unions offer financing on their own repo inventory. Others require buyers to pay cash or arrange financing elsewhere.

Financing may depend on:

- Credit history

- Income

- Down payment

- Motorcycle age

- Loan amount

- Title status

- Lender policy

Ask about financing before submitting an offer. Some lenders require full payment within a short period after accepting a bid.

Where to Find Repo Motorcycles for Sale

Banks and credit unions often advertise repossessed motorcycles on their websites. However, searching hundreds of individual lender websites can take significant time.

RepoFinder helps buyers locate motorcycles offered by banks, credit unions, and other financial institutions throughout the United States. Buyers can compare available motorcycles and contact the listed seller directly.

Browse current repo motorcycles for sale

Tips for Finding the Best Repo Motorcycle Deal

- Compare several motorcycles before making an offer.

- Verify the seller through the bank or credit union’s official contact information.

- Inspect the motorcycle in person whenever possible.

- Confirm the VIN and title status.

- Research the motorcycle’s market value.

- Estimate all immediate repairs.

- Ask about seller and auction fees.

- Calculate transportation costs before bidding.

- Read the sale terms carefully.

- Set a maximum price and avoid emotional bidding.

Frequently Asked Questions

How much do repo motorcycles usually cost?

Repo motorcycles may cost anywhere from about $2,000 for an older beginner motorcycle or dirt bike to more than $25,000 for a newer touring motorcycle or trike. Actual prices depend on age, mileage, condition, brand, location, and demand.

Are repo motorcycles cheaper than dealer motorcycles?

They can be. Banks and credit unions may price repossessed motorcycles competitively because they want to recover loan balances and reduce storage costs. However, buyers should compare repair needs, warranties, fees, and transportation costs.

How much can I save on a repo motorcycle?

There is no standard repo discount. Savings vary by motorcycle, lender, condition, and local market. Calculate the total purchase cost before comparing the repo with dealer and private-party listings.

Why are some repo motorcycles so cheap?

A low price may reflect age, high mileage, cosmetic damage, mechanical problems, missing keys, limited documentation, or the lender’s desire to sell quickly. Inspect the motorcycle before assuming the low price represents a bargain.

Do repo motorcycles have clean titles?

Many repossessed motorcycles have standard titles. However, buyers should verify the title for salvage, rebuilt, flood, junk, or other branding before purchasing.

Can I finance a repo motorcycle?

Some banks and credit unions offer financing on their repossessed motorcycles. Other sellers require cash or outside financing.

Are repo motorcycles sold as-is?

Most lenders sell repo motorcycles as-is and without a warranty. Buyers should inspect the motorcycle and budget for possible repairs.

Does RepoFinder sell the motorcycles?

RepoFinder helps buyers locate motorcycles offered by banks, credit unions, and other sellers. The listed financial institution or seller controls the price, sale terms, payment, title transfer, and pickup process.

Final Thoughts

Repo motorcycles commonly range from a few thousand dollars for older entry-level bikes to more than $25,000 for newer touring motorcycles and three-wheel models. However, the asking price tells only part of the story.

The best buyers compare market values, inspect the motorcycle, verify the title, estimate repairs, and calculate the total transaction cost. A carefully selected repo motorcycle can provide excellent value, but a low-priced bike with major repair or transportation expenses may cost more than expected.

Browse current inventory, compare several options, and contact the seller directly before making an offer.

View repo motorcycles for sale from banks and credit unions