Why Used Cars Are Still So Expensive in 2025

This entry was posted in Blog and tagged car buying, car shopping, cheap cars, online car shopping on .

When purchasing a vehicle, many drivers think about the immediate costs, down payments, financing, insurance, and routine maintenance. But what often gets overlooked is how to safeguard that investment in the long run. Vehicles are complex machines with thousands of parts, any of which can fail. Repair costs can quickly add up as a car ages and factory warranties expire. That’s where long-term vehicle protection plans come in, providing peace of mind and financial stability for years of ownership.

Long-term protection plans, often referred to as extended warranties or vehicle service contracts, are designed to pick up where the manufacturer’s warranty leaves off.

While factory warranties typically last only a few years, these plans can extend coverage well into the vehicle’s lifespan, covering costly repairs that would otherwise fall on the owner. Drivers considering options can explore resources such as https://www.chrysler-factory-warranty.com/mopar-extended-warranty/ to understand the range of available plans, from basic powertrain coverage to comprehensive “bumper-to-bumper” protection. These plans often cover systems like engines, transmissions, and electrical components, as well as offering perks like roadside assistance and rental car reimbursement.

By choosing the right plan, vehicle owners gain a safety net against unpredictable repair bills.

One of the biggest benefits of a protection plan is the financial predictability it brings. Repair costs for modern vehicles can be shockingly high due to advanced technology, electronics, and labor-intensive work. A single repair, such as replacing a transmission, can run into thousands of dollars, an expense most drivers aren’t prepared for.

With a protection plan, drivers can spread these costs into manageable payments or upfront fees, ensuring their budgets remain steady. The result is less financial stress and fewer surprises. For many owners, the peace of mind alone justifies the investment.

Understanding the types of repairs commonly covered by vehicle protection plans highlights their true value. Even reliable vehicles eventually experience wear and tear, and when major systems fail, repair bills climb quickly.

Some of the most costly and frequent repairs include:

Having these covered under a protection plan means drivers avoid dipping into emergency savings or taking on debt just to keep their car running.

Beyond financial coverage, long-term vehicle protection plans often include added conveniences that improve the ownership experience. These extra benefits are sometimes overlooked but can make life significantly easier when unexpected problems arise.

Key perks to look for include:

These extras enhance the value of protection plans, making them a financial safeguard and a practical support system for daily life and long-distance travel.

Another overlooked advantage of long-term protection plans is how they affect resale value. Vehicles with transferable coverage are often more attractive to buyers because they come with added security. For someone purchasing a used car, knowing that key components are still covered can be a deciding factor.

For sellers, this translates into better offers and faster sales. It demonstrates that the vehicle has been cared for properly, as buyers often associate warranty coverage with responsible ownership. Protection plans, therefore, don’t just save money on repairs; they can help owners recoup more value when it’s time to sell.

Of course, like any investment, long-term vehicle protection plans come with costs that must be weighed against potential benefits. Not every driver will need comprehensive coverage, and plans vary widely in terms of pricing and inclusions. It’s important to evaluate personal driving habits, how long you plan to keep your vehicle, and your tolerance for financial risk.

Drivers who put a lot of miles on their cars, or who plan to keep them well past the factory warranty, often see the most value. Conversely, those who trade in vehicles frequently may benefit from shorter-term plans. Taking the time to compare options, read the fine print, and ask questions ensures that you choose a plan aligned with your specific needs.

Long-term vehicle protection plans offer far more than repair coverage; they provide peace of mind, financial predictability, and added value at resale. By covering common costly repairs, offering perks like roadside assistance, and boosting buyer confidence, these plans play a crucial role in protecting one of life’s most significant investments. For drivers committed to keeping their vehicles reliable and stress-free, exploring the right protection plan can be one of the smartest decisions they make.

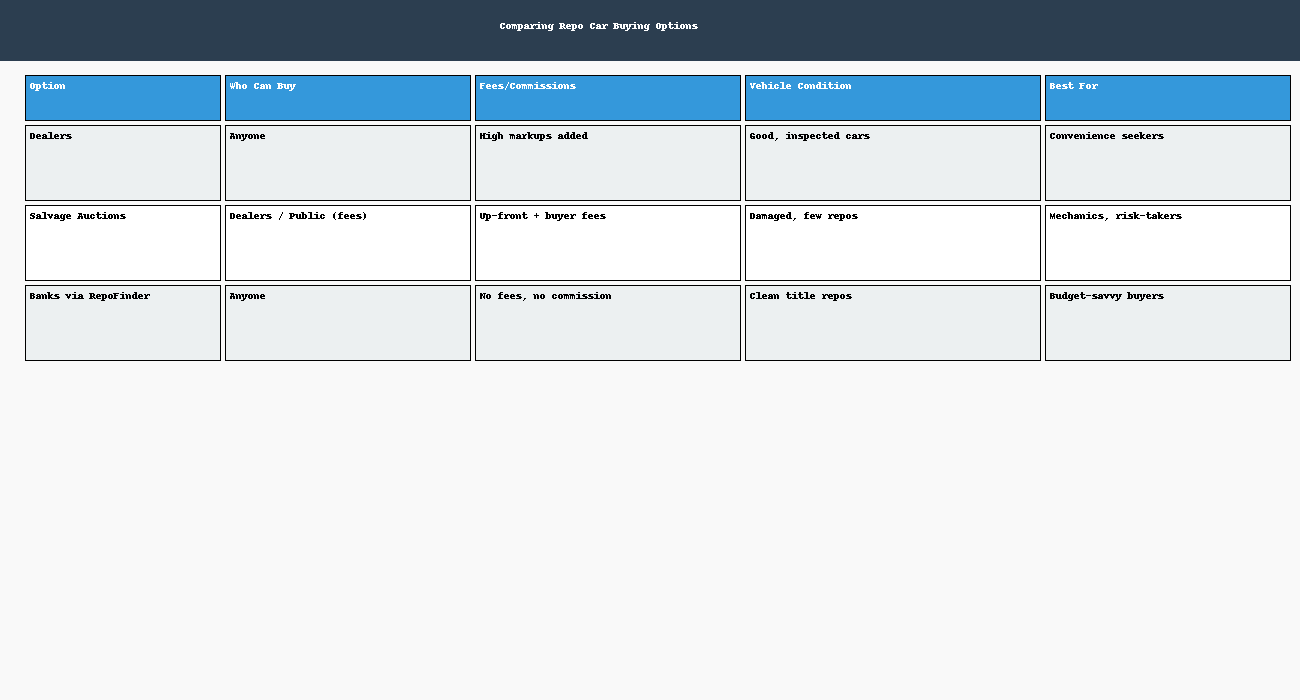

Many people want to buy a repossessed car for less money. But they quickly hit roadblocks. Some think a dealer’s license is required. Others get stuck paying fees at salvage auctions.

The truth? You don’t need a dealer’s license to buy a repo car. You just need to know where to look.

This guide explains three common ways people try to buy repos. You’ll see why dealers and salvage auctions rarely save you money. Finally, you’ll learn the best method: buying directly from banks and credit unions using RepoFinder.com.

A repossessed car is taken back by a lender after the owner stops making payments.

Banks and credit unions want to sell quickly to recover their money. That urgency can mean savings for buyers.

Most repo cars are still in good condition. Many have clean titles.

Many believe you must be a dealer to buy repos. That’s only true at certain auctions.

Dealer-only auctions restrict public access. But banks and credit unions often sell repos directly to anyone. No license needed.

There are three paths most buyers follow, only one (#3) is actually getting you the BEST deal:

Buying from car dealers who claim to sell repos.

Buying at salvage auctions.

Buying directly from banks and credit unions.

Dealers love to advertise “repo cars.” But those cars usually already passed through auctions.

The dealer adds markups and commissions. Those extra costs erase the savings.

Pros:

Cars are often inspected and ready to drive.

Easy financing options may be available.

Cons:

Higher prices from dealer markups.

You don’t deal directly with the bank.

Bottom line: Buying from a dealer is simple but not the cheapest way.

Many people think auctions are full of repos. In reality, most auction cars are wrecked, flooded, or heavily damaged.

Public bidders must often pay up-front registration fees. Then more fees if they win.

Some repos appear at these auctions, but they’re usually in rough shape.

Pros:

Large selection of vehicles.

Online access allows bidding from anywhere.

Cons:

Many auctions are dealer-only.

Fees add up quickly.

Repos are rare, and cars are often damaged.

Bottom line: Auctions work for risk-takers or mechanics but not everyday buyers.

This is the best path for most people.

Banks and credit unions repossess cars every month. They need to sell quickly. Their repos are often in good shape.

RepoFinder.com lists these lenders for free. Buyers deal directly with the bank. No middleman, commission, or extra fees.

Pros:

No dealer license required.

No fees or commissions.

Clean titles and lower prices.

Direct communication with the seller.

Cons:

Inventory can be limited.

Cars may sell quickly.

Bottom line: Buying direct from lenders is the simplest and most cost-effective way.

Visit RepoFinder.com.

Select your state.

Choose a bank or credit union.

Browse their repo listings.

Contact the lender directly.

Inspect the car before buying.

Ask about financing.

Make your offer.

Complete the paperwork.

Drive away with your deal.

Always check the title before buying.

Compare prices with local dealers.

Move quickly as good repos sell fast.

Inspect in person when possible.

Do repos have clean titles?

Usually yes when they are sold directly by banks. Many are still in great shape.

Can I test drive a repo car?

In most cases you can. Ask the bank.

What if I don’t live near the bank?

Most lenders allow online offers and vehicles can be shipped.

Are repos always a good deal?

Often yes. Especially when buying directly.

You don’t need a dealer’s license to buy a repossessed car.

Avoid dealers that add markups. Avoid salvage auctions that pile on fees and sell cars that are heavily damaged.

The smartest move is buying directly from banks and credit unions. RepoFinder.com makes this easy by listing lenders in every state.

Take action today. Start your search at RepoFinder.com and see how much you can save.

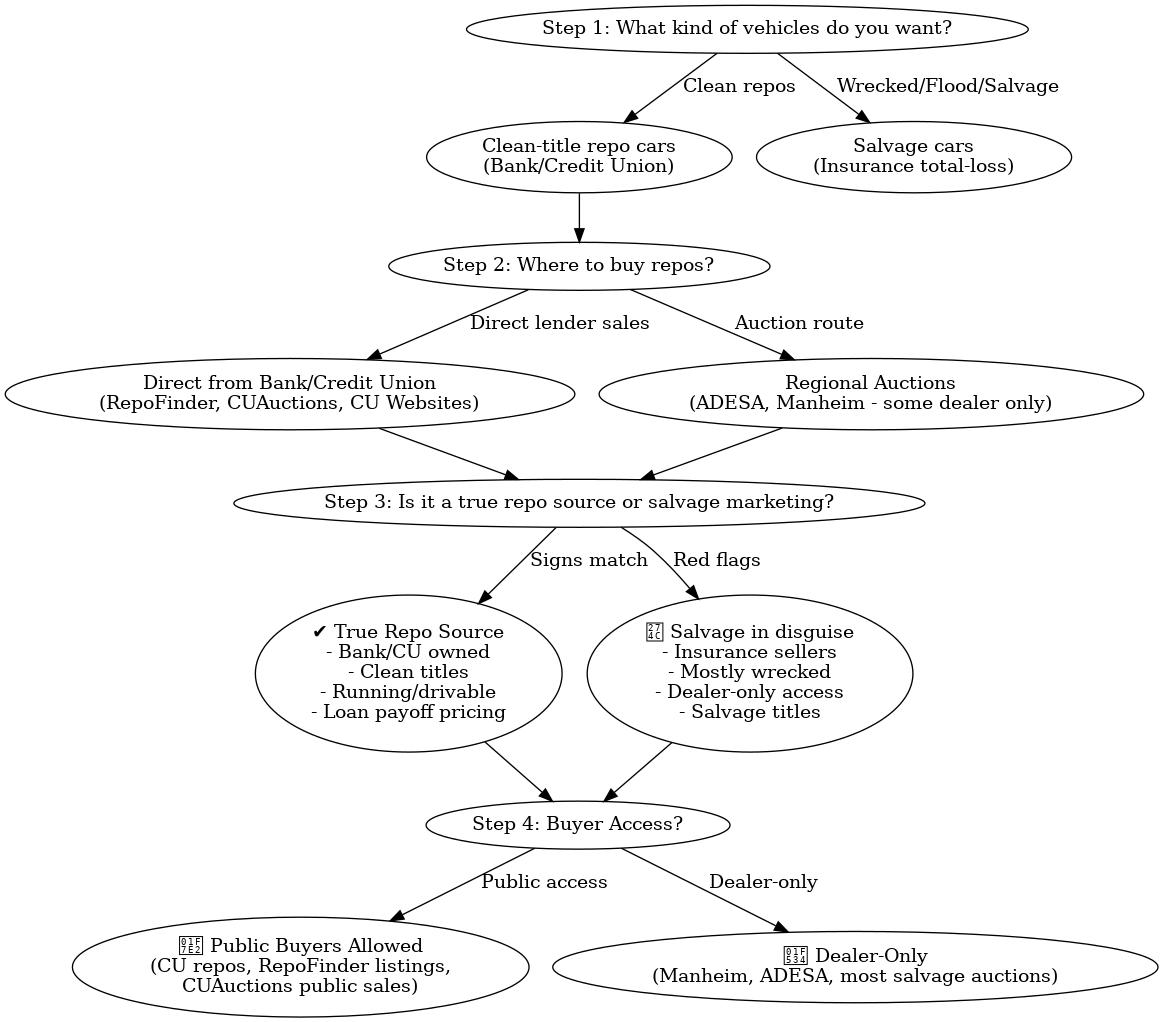

Unfortunately, a lot of big players in the automotive sales arena are using the term “repo car” to bait-and-switch buyers into buying “salvage cars”. These are large auction houses that primarily sell wrecked and damaged vehicles. Sure they may sell a few repos from time-to-time, but a deeper dive shows they’re a lot heavier on smoke and mirrors than actual repo car deals.

Here’s a repo car buyers decision tree to help you sort this all out:

🚗 Clean-title repos (bank/credit union repos) → Go to Step 2

🚧 Wrecked, flood, or insurance total-loss cars → That’s salvage, check Copart / IAAI / RideSafely

🏦 Directly from the lender (bank or credit union)

✅ Look on RepoFinder.com (directory of banks/CUs in all 50 states)

✅ Check lender websites (look for “Vehicles for Sale” or “Repos”)

✅ Watch for links to CUAuctions (credit union auction hub)

🏢 Through an auction house (but clean repo inventory)

✅ Some regional auctioneers (e.g., ADESA, Manheim) sell clean repos — but many are dealer-only

⚠️ Public buyers may need a broker or find “public auctions” only

Site is run by a bank, credit union, or their auction partner

Titles are clean (unless disclosed otherwise)

Vehicles are typically late-model, good condition, running/drivable

Prices are usually “loan payoff + fees” — not inflated retail

❌ Signs it’s salvage in disguise:

Site is dominated by wrecked, flood, or non-running vehicles

Primary sellers are insurance companies, not lenders

Buzzwords like “repo, clean, fixer-upper” sprinkled across mostly salvage inventory

Requires dealer license or broker just to bid

🟢 Public buyers allowed → Credit union repos, RepoFinder listings, some CU Auctions, a few public regional auctions

🔴 Dealer-only → Manheim, ADESA, most salvage platforms (need broker or license)

If you want clean repo cars, skip Copart, IAAI, RideSafely (salvage-focused).

Start at RepoFinder → browse banks/CUs in your state.

Check if they sell direct-to-public or use CUAuctions.

If it isn’t sold DIRECTLY by the bank there is a middleman making a commission or fee.

sort through the smoke, mirrors, and nonsense, and find an actual clean title repo car from a bank.

Buying a motorcycle is one of those life milestones that feels big. You’re not just getting wheels—you’re getting freedom, wind in your face, and maybe even a new nickname at bike night.

But before you start shopping for leather jackets and sunglasses, you have to face a question: where should you buy your bike?

You really have three main options:

From a dealer

From a private seller

From a bank repo sale

Each option has fans and haters. Some swear by dealers, others insist private parties give the best deals, and a growing number of smart buyers are finding out that bank repos can be goldmines.

This post will walk you through the pros and cons of each choice, with real talk, easy explanations, and a dash of snark. By the end, you’ll know exactly where you should buy your next motorcycle.

Dealers are like the big-box stores of motorcycles. Walk in, and you’ll see shiny new Harleys, Hondas, Yamahas, and maybe even a Ducati or two. Everything is clean, polished, and ready to ride.

Selection – Dealers carry multiple makes and models. Want a Honda Gold Wing? Or maybe a Yamaha R1? You’ll probably find both.

Financing – Dealers almost always offer financing. If you don’t want to shell out $10k+ in cash, this is helpful.

Warranty – Many new bikes come with a manufacturer warranty. That’s peace of mind if you’re not mechanically inclined.

Paperwork made easy – Title, registration, taxes—all handled by the dealer.

Dealer markup – You’ll pay more, sometimes thousands more. That’s the price of convenience.

Hidden fees – Setup fees, freight charges, documentation fees. Dealers can nickel-and-dime you until you need another loan.

Less room for negotiation – You might shave a little off the price, but most dealers stick close to MSRP.

New riders who want convenience, financing, and someone else to do the paperwork. Or anyone who wants a shiny new Harley-Davidson without worrying about whether the last owner treated it like a stunt bike.

Craigslist. Facebook Marketplace. That one coworker who says his cousin has a sweet Kawasaki Ninja for sale. Private-party sales feel more personal and are often cheaper. But they’re also where the sketchiest deals happen.

Lower prices – No dealer markup. If a bike’s worth $6,000, you might snag it for $5,000.

Negotiation power – Most private sellers expect haggling. Bring cash, and you might get an even better deal.

Unique finds – You might stumble across rare bikes or well-loved classics you’ll never see at a dealer.

No warranty – Once you buy it, it’s yours, problems and all.

Risk of scams – Fake titles, rolled-back odometers, or worse.

Paperwork is on you – You’ll need to handle the title transfer, taxes, and registration yourself.

Condition is a gamble – Some owners take meticulous care of their bikes. Others think oil changes are optional.

Experienced riders who know what to look for, aren’t afraid of turning a wrench, and don’t mind chasing down paperwork at the DMV.

A repo (short for “repossessed”) is a motorcycle the bank took back after the owner stopped making payments. Banks don’t want to store motorcycles, they want their money back. That means repo bikes often sell for less than market value.

Lower prices – Banks usually price repos to move fast. Bargains are everywhere.

Clean titles – Unlike salvage auctions, repo bikes almost always come with clean titles.

No middleman – Sites like RepoFinder.com connect you directly to banks and credit unions. No dealers. No commissions. No junk fees.

Bank perks – Repos can be almost like buying from a dealer. Banks handle paperwork and often provide financing too, without charging extra fees.

Sold as-is – Don’t expect warranties or service records. The bank knows as much as you do.

Limited selection – Inventory depends on who defaulted that month. Some weeks it’s Harleys, other weeks it’s Yamahas.

Competition – Once people realize how cheap repo bikes are, good deals get snatched fast.

Smart buyers who want a deal but also like the peace of mind of bank-handled paperwork and financing. Basically, the best of both worlds.

Here’s an infographic-style comparison of the three options.

Dealer vs. Private Party vs. Repo

| Feature | Dealer ✅ | Private Party ✅ | Bank Repo ✅ |

|---|---|---|---|

| Price | $$$$ | $$ | $ |

| Financing | Yes | Rare | Yes (through bank) |

| Warranty | Often | No | No |

| Paperwork | Handled | Buyer’s job | Bank handles |

| Fees | High | Low | None at RepoFinder |

| Negotiation | Limited | Good | Possible |

| Selection | Wide | Hit-or-miss | Varies monthly |

| Risk Level | Low | Medium-High | Medium |

When choosing where to buy, think about:

Budget – Can you handle dealer markups, or do you want repo savings?

Experience – Do you know how to inspect a used motorcycle?

Risk tolerance – Do you need peace of mind, or are you okay rolling the dice?

Paperwork – Do you want someone else to do it, or are you cool with the DMV?

If you’re leaning toward a repo, you’ll need a place to find them. That’s where RepoFinder.com comes in.

Here’s why RepoFinder is different:

Direct-to-bank listings – No dealers, no middlemen.

Free to use – Unlike auction sites, there are no fees or commissions.

Bank support – The bank usually handles your paperwork, just like a dealer would.

Financing available – Many banks offer in-house motorcycle loans for repo sales.

It’s like a dealer without the markup, or a private seller without the risk. Basically, the smart rider’s shortcut to a better deal.

Let’s recap:

Dealer – Best for convenience, financing, and warranty, but you’ll pay more.

Private party – Best for negotiators and bargain hunters, but risky if you’re not careful.

Repo at a bank – Best for savvy buyers who want low prices, clean titles, and bank-handled paperwork—without the dealer markup.

So if you’re serious about getting the most bike for your buck, skip the drama and head to RepoFinder.com. You’ll find Harleys, Hondas, Yamahas, and Kawasaki sitting on bank lots, just waiting for a new rider.

Because the only thing better than riding your dream motorcycle is knowing you didn’t get ripped off buying it.

Modern RV buyers want more than wheels and a bed. They want a connected lifestyle. People expect internet, smart devices, and tech comforts everywhere, even while camping. The RV industry has responded with new innovations that blend mobility and modern living. In this guide, we’ll explore how technology makes RVs smarter, why connectivity is so important, and how shoppers can save money by buying repossessed RVs through banks and credit unions on RepoFinder.com.

RVs once meant leaving technology behind. Today, that has changed. Families, digital nomads, and retirees want the same tech on the road that they enjoy at home. People want to stream movies, take Zoom calls, and manage smart devices from the wilderness. With remote work and mobile living on the rise, strong connectivity is no longer optional—it’s essential.

Here are the most in-demand features RV buyers look for today:

Starlink has transformed RV life. It provides high-speed satellite internet almost anywhere. Remote work and streaming are now possible deep in the mountains or deserts.

Campgrounds often have weak Wi-Fi. Boosters grab that signal and strengthen it, allowing smoother browsing and streaming.

Smart thermostats let you adjust heating and cooling from your phone. No more rushing back to change the temperature.

RVs are now equipped with solar panels and long-lasting batteries. These let owners camp off-grid while still enjoying power.

Owners want to keep their RVs safe. Cameras, alarms, and locks controlled by apps give peace of mind when parked.

Some RVs have Alexa or Google Assistant integration. Owners can turn lights on or off with a simple command.

Flat-screen TVs, surround sound, and streaming systems make RV living fun for families and travelers.

Apps can now monitor tire pressure, water tanks, and battery life. This prevents surprises while traveling.

Modern kitchens in RVs include Wi-Fi enabled refrigerators and convection ovens. Cooking on the road feels like home.

Shoppers no longer have to choose between adventure and comfort. Modern RVs combine mobility with smart living. With these upgrades, people can:

The mix of freedom and technology has created a new lifestyle. RVs are now mobile homes in every sense of the word.

Of course, all this technology adds cost. New RVs with advanced systems can be very expensive. That’s why many smart shoppers look for better deals. One of the best ways to save money is by buying repossessed RVs.

When people stop making payments, banks and credit unions repossess RVs. These repos are often sold at discounted prices. Unlike dealers, banks want to sell quickly. That means buyers can often save thousands.

The easiest way to find these repos is by using RepoFinder.com. RepoFinder lists repossessed RVs directly from banks and credit unions nationwide. There are no middlemen, commissions, or fees.

On RepoFinder, you’ll find:

Each listing comes directly from a financial institution. This helps shoppers avoid hidden dealer tricks and inflated prices.

Image Concept: An RV shown from the side. Arrows point to features with text labels:

RV shoppers in 2025 want more than a vehicle. They want a connected home on wheels. Technology like Starlink, Wi-Fi boosters, and smart systems have redefined RV life. Comfort and mobility now go hand in hand. But buying new can be costly. That’s why RepoFinder is the best way to save. By buying directly from banks and credit unions, you can enjoy modern tech and keep your budget in check.

Buying a used car used to mean going to a dealership, walking a lot, and haggling with salespeople. Not anymore. Today, more people are shopping online for used cars. They want clear prices, fast info, and less stress.

This trend isn’t just for dealerships. Banks and credit unions are getting in on it too. They are now posting their repossessed cars online. Some are even offering direct sales. You can now find these bank-owned vehicles on websites like RepoFinder.com.

In this article, we’ll show how banks are entering the digital car market. We’ll also explain why this is good news for buyers like you.

Shopping for a car online is faster and easier. A few years ago, only about 1 in 10 people bought a car online. Today, it’s closer to 1 in 4. And that number keeps growing.

Why the change?

Buyers want to compare cars from home.

People don’t want to deal with pushy sales tactics.

Many now trust online listings with photos and history reports.

With so much moving online, it makes sense that banks are joining the trend.

Banks and credit unions give auto loans. If a person stops paying, the bank takes the car back. This is called a repossession, or repo for short.

The bank doesn’t want to keep the car. It wants to sell it quickly and get back some of the loan money.

In the past, banks used auctions or local dealers. But now they’re going digital. They want to sell directly to you — the buyer — using websites like RepoFinder.com.

This cuts out the middleman. It also helps the bank move the car faster.

RepoFinder.com is a free website that lists bank-owned vehicles for sale. It works with banks and credit unions all across the U.S. These financial institutions post repossessed cars, trucks, RVs, boats, and more.

Here’s what makes RepoFinder different:

It doesn’t charge buyers any fees.

It doesn’t sell the cars itself. It connects you with the actual bank.

It’s one of the only sites that lists bank repos directly to the public.

You don’t need to sign up to browse. Just pick your state and start exploring.

Check out the vehicle listings by state on RepoFinder to see what’s available near you.

Banks are realizing that more people want to shop from home. So they’re improving how they market repossessed vehicles.

Here’s what you can expect:

Online photos: You can see the car before visiting.

Basic info: Year, make, model, mileage, and condition.

Contact details: You talk directly with the bank, not a dealer.

Financing options: Many banks offer financing on their own repos.

Some banks also post repos on their own websites. Others prefer to list them on marketplaces like RepoFinder to reach more buyers.

Carlos, a college student in Texas, needed a cheap but reliable car. He didn’t want to get ripped off by a used car dealer. His friend told him to check out RepoFinder.

Carlos searched his state and found a 2017 Honda Civic listed by a local credit union. It had 84,000 miles and was listed at $9,300 — about $2,000 less than similar cars online.

He called the bank. They let him come see the car and test drive it. The car needed new tires, but everything else checked out.

Carlos bought the car for $8,900 after a little negotiation. The credit union even helped him with a low-interest loan.

He’s now driving to school debt-free and tells everyone about his experience.

Bank repos are often cheaper than dealer cars. Why?

The bank isn’t trying to make a profit.

They just want to recover the loan amount.

No dealer fees or markups.

Other benefits include:

Faster sales: Banks are motivated to sell quickly.

Clean titles: Most bank-owned vehicles have clear titles.

Financing: Some banks offer low-rate loans to buyers.

Still, it’s smart to inspect the car first. Most are sold as-is, which means no warranty. But many repos are in good shape — especially ones that were recently taken back.

Not always. Many banks post repos at a fixed price. Some may accept offers. Others might use sealed bids. It depends on the bank.

Yes, often you can. Many banks offer loans on their own repos. They may even offer lower rates to help sell the car faster.

Some banks inspect their vehicles before listing them. Others sell them as-is. You can always ask for a test drive or bring a mechanic to check it out.

Yes. Many banks will let you buy even if you live out of state. But you may need to arrange pickup or transport.

Repos are usually final sales. Always do your research first. Check the car history and condition before you commit.

Compare prices: Look at other listings on websites like Kelley Blue Book or Edmunds.

Get a vehicle history report: Ask the bank for a report or use services like Carfax.

Ask questions: Don’t be afraid to contact the bank directly.

Inspect the vehicle: Always try to see it in person or have it looked at.

Know your budget: Just because it’s cheaper doesn’t mean you should overspend.

Check title status: Make sure the title is clean and ready to transfer.

Used car prices have gone up in recent years. Even 3-year-old cars are now over $30,000 on average.

Buying a repo can help you save thousands. You skip the dealership and deal directly with the bank. This means:

No sales commissions

Lower sticker prices

Easier access to financing

And when you use RepoFinder.com, you’re seeing the listings banks want buyers to find. Not random auction leftovers.

The used car market is changing fast. Buyers want better tools, more trust, and real value. Banks know this. That’s why they’re moving online and marketing their repos to regular people like you.

RepoFinder makes it easy. It’s a simple, free tool that connects you with banks across the country.

And as digital car shopping grows, expect even more banks to list repos directly online.

You don’t need to be a car expert to get a great deal. You just need the right info and tools.

Banks now sell repos online. Sites like RepoFinder help you find these deals in just minutes.

If you’re shopping for a used car, don’t skip this step. You could find your next ride at a price way below market value.

Start browsing repos near you today at RepoFinder.com.

Want to see how digital retailing is growing? Check out this industry report from Spyne.

How to protect your wallet and avoid common dealership traps in 2025

Jessica saved for months. She found a used SUV online listed at $18,995.

When she got to the dealership, they added $2,300 in fees. She walked away upset.

Many buyers face the same problem. Dealers often show low prices online.

But the real cost can be much higher once they add hidden charges.

In 2025, these tricks are getting worse.

This guide will help you spot hidden fees and avoid common dealership traps.

Hidden fees are charges the dealer adds without clear warning.

They are not always listed in the online ad.

You might hear the dealer say, “This is standard” or “It’s already on the car.”

But that doesn’t make it right.

VIN Etching Fee: $200–$400 for engraving the vehicle ID on windows

Fabric Protection: A $300 spray they say keeps seats clean

Paint Protection: $500 for a wax-like coating

Documentation Fee (“Doc Fee”): Paperwork costs; sometimes over $1,000

Market Adjustment Fee: A random price hike just “because demand is high”

Service Contracts or Extended Warranties: You didn’t ask for it—but it’s in your payment

These fees can add $600–$2,500 to the car’s cost. That’s money you didn’t plan to spend.

Used cars are expensive in 2025. The average 3-year-old car costs over $30,000.

Why? A 25% tariff on imported cars and parts raised prices everywhere.

More people are turning to used cars, making them harder to find.

Dealers know this. Some are using tricky fees to boost profits.

Even though the FTC tried to make new rules, courts blocked them.

Now, most protection comes from state regulators—and they can’t catch everything.

A recent survey found:

82% of buyers would back out if fees jumped 25%

60% would cancel a deal if fees rose just 5%

This shows how sensitive buyers are. And why it’s important to stay alert.

You see a great price online. But when you get to the dealership, they say,

“This includes our protection package.”

It might be window tint, wheel locks, or a $1,000 anti-theft system.

It wasn’t optional. And now they claim it’s already installed.

Tip: You don’t have to pay for things you didn’t request.

They promise a great rate online. But once you’re in the office, they say,

“You didn’t qualify for that rate.”

Then they offer a new loan with a higher rate and longer term.

This adds thousands in interest.

Tip: Get pre-approved at a credit union or bank before visiting the dealer.

Some dealers show prices without destination fees, prep charges, or dealership add-ons.

You think it’s $18,000—but it turns into $22,000 fast.

Tip: Always ask for the full “out-the-door” price.

They hand you a thick contract and say, “It’s all standard. Just sign here.”

Don’t fall for it. You might be agreeing to fees you don’t understand.

Tip: Take your time. Read everything.

Sometimes you’ll see charges like “Nitrogen tire fill” or “Theft Recovery System.”

These often add no real value. But the cost can be high.

Tip: Ask what each fee is. Say no to the ones you don’t want.

You have more power than you think. Here’s how to use it:

This price includes everything; car, taxes, title, and fees.

If they won’t give it, walk away.

This paper shows every fee. Look for things you didn’t agree to.

If it looks wrong, ask questions.

Some fees are real and required:

Sales tax

Title and registration fees

State inspection fees

But many others are just fluff.

You can say, “Take this off,” even if they claim it’s already installed.

If they won’t remove it, ask for a discount.

Having a second set of eyes helps. Especially if this is your first big purchase.

We asked car experts what buyers should do in 2025. Here’s what they said:

Time your visit: Go at the end of the month. Dealers are eager to hit sales goals.

Shop mid-week: Weekdays are quieter. You’ll get more attention.

Get pre-approved: Your bank or credit union may offer better rates.

Shop repo cars: Banks sell cars they’ve repossessed. These often come with no added fees.

✅ You can find these cars at RepoFinder.com.

“I found a 2017 pickup listed at $24,995. When I got there, it jumped to $28,300.

They added a ‘dealer prep fee’ and ‘market adjustment.’ I left. Two days later, they called and dropped the fees. I ended up buying it for the original price.”

“I didn’t understand the paperwork and signed fast. Later I saw I paid $899 for ‘etching.’ I called and they wouldn’t remove it. Lesson learned—read every line.”

“I used RepoFinder to get a car from a local credit union. No games. They gave me the full price up front. I saved $2,000.”

No. Sales tax, title, and registration are real. But many add-ons aren’t needed.

Buyers are paying about $640 in surprise charges this year—some even more.

Yes. Even if it’s already installed, you can ask them to remove the charge or discount the price.

It’s engraving your car’s VIN on the windows. It helps with theft recovery, but it’s often overpriced.

Try banks and credit unions. Start with RepoFinder.com to see repos in your area.

[Infographic description — if image not viewable]

| Fee Type | Average Cost | Worth It? |

|---|---|---|

| VIN Etching | $200–$400 | Usually No |

| Fabric Protection | $300 | Not Needed |

| Paint Sealant | $500 | Not Needed |

| Doc Fee | $500–$1,100 | Sometimes Legit |

| Market Adjustment | $1,000+ | Just a Markup |

| Theft System | $600–$900 | Ask Before Buying |

| Nitrogen Tire Fill | $100 | Not Worth It |

You don’t have to accept every fee. Ask questions. Take your time.

If something feels wrong, trust your gut and walk away.

The used car market in 2025 is tough, but you can still win.

Just stay sharp, stay calm, and know what to watch for.

And if you want to avoid tricky fees altogether?

Start your search with a bank or credit union repo at RepoFinder.com.

.

Buying a used car can feel confusing. Prices vary. Dealers use tricks. Auctions move too fast.

That’s where RepoFinder.com comes in. We help regular people find real repossessions for real savings.

You don’t need to be a dealer or go to a high energy auction where you’ll feel like a fish out of water. You just need to know where to look.

We’ll explain why RepoFinder.com is one of the best ways to find a used vehicle today.

RepoFinder.com is a free website that helps you find repossessed vehicles, boats, RVs, and property.

We’re different from other car sites. We don’t sell cars or run auctions. We don’t charge and dealer fees because we’re not a dealer or an auction house.

Instead, we connect you directly to banks and credit unions who are selling their repossessed items.

These banks want to sell fast. That means you can often get a better deal.

Let’s break it down. Here are the top 3 reasons people trust RepoFinder.com when shopping for used cars.

Most people don’t know this, but banks and credit unions often have vehicles they’ve repossessed from borrowers.

These repos are often:

Well-maintained

Sold at a discount

Ready for quick sale

Banks are not car dealers. They just want to get their money back. That’s good news for buyers like you.

At RepoFinder.com, you don’t buy from us. You buy straight from the bank.

This is different from:

Auction sites that require bidding

Dealers who mark up prices

Brokers who add middleman fees

Our site lists real links to each bank or credit union’s repo inventory. You go straight to the source.

You can call them. Visit them. Even make offers directly.

And yes—many banks even offer financing on their own repos. (You can read more about that here.)

This means you may get better loan terms than at a dealership.

RepoFinder.com is more than a search bar. It’s a map of the entire country’s repossessions.

Every state. Hundreds of banks and credit unions. All in one place.

You don’t have to search site after site. We’ve already gathered the links for you.

Just visit our state map. Click your state. You’ll see all local listings and banks with repos.

For example:

In Texas? You’ll see dozens of credit unions with repos.

In Florida? Many local banks list boats and cars weekly.

In California? You’ll find credit unions with clean-title SUVs and sedans.

You don’t need to know a bank’s name. You just click the state and browse.

It’s simple. It’s fast. And it’s always growing.

Let’s be honest. Many car-buying sites are full of tricks.

They make you sign up. Perhaps they sell your info. Most likely they’ll push you toward high-priced dealers.

RepoFinder.com does none of that.

No dealer fees

No commissions

No middlemen

We’re not trying to sell you a car. We’re here to show you where the deals are at your local banks.

You just contact the seller (a bank) and make an offer. It’s that simple.

Many listings are “first come, first served.” That means you can move fast—and save big.

Besides cars and trucks, you can also find:

Boats

RVs and campers

Motorcycles and ATV’s

Real estate

Equipment and machinery

Banks repossess more than cars. They sometimes list homes, jet skis, even tractors.

These items are usually listed on the bank’s own site. But we link you there.

That means you’re seeing true repo prices—not marked-up ones.

Buying a repo does come with some things to watch out for. Here are a few:

Most repos are sold as-is

You may not get a warranty

Inspections are sometimes limited

But remember—this is the same deal the dealers get. They buy repos at low prices and resell them.

With RepoFinder, you get that same access, but you cut out the dealer markup.

If you’re smart and do a little research, you can save thousands.

We always suggest:

Running a vehicle history report

Asking if test drives are allowed

Getting a mechanic’s opinion if possible

Step 1: Visit RepoFinder.com

Go to www.RepoFinder.com. It works on phones, tablets, and computers.

Step 2: Click Your State

Use the state map or the state list. Click where you live or want to shop.

Step 3: Browse the Repo Listings

Each bank or credit union has a link. Some take you to car listings. Some let you make offers online.

From there, you’re in control. You contact the seller. It’s you who asks about the vehicle… and it’s still you (and the bank) who work out your deal.

RepoFinder is great for:

People who want to avoid dealers

Buyers looking to save money

Families who need a second vehicle

People who can wait for the right deal

If you need a car today, you might go to a dealer. But if you want a better deal, RepoFinder gives you a smarter option.

That’s the best part—we don’t charge buyers anything.

Some banks pay a small fee to be listed. But most of the site is totally free.

Our goal is to help people find hidden deals. We believe in transparency and no gimmicks.

RepoFinder is supported by ads like most free websites on the internet. We also provide an enhanced service at RepoFinder Pro with no ads and other perks.

Here’s how to get the most out of RepoFinder:

Check weekly: Listings change fast

Be flexible: You may find better deals in nearby states

Ask about financing: Many banks offer it on their own repos

Move fast: Good deals don’t last long

Stay patient: Waiting for the right deal can pay off big

“I found my truck through a credit union linked on RepoFinder. Saved over $5,000 compared to dealer prices!” – Mike B., Colorado

“No auctions, no fees. I found a clean-title boat for under market value. Super easy.” – Janice R., Florida

“I used to flip cars. Now I just use RepoFinder to find my next ride.” – Paul L., Texas

Do I need a dealer’s license?

No. Most repo listings are open to the public.

Are the vehicles clean title?

Most are, but check with the bank. Some may be rebuilt or salvage.

Can I test drive the car?

Sometimes, yes. It depends on the seller. Ask before making an offer.

Do I have to go to an auction?

Nope. RepoFinder shows you non-auction repos available to the public.

What if I live in a small state?

Browse nearby states too. Many banks sell to out-of-state buyers.

RepoFinder.com is simple, free, and powerful.

We help people:

Find repossessions the public can actually buy

Connect directly to banks and credit unions

Avoid auctions, scams, and overpriced dealers

In a world full of tricks and hidden fees, we keep it easy.

If you’re buying a car, boat, RV, or even a home—start with RepoFinder.

You might be surprised what you find.

Browse repos by clicking your state on our Repo Map. It only takes a few seconds.

Just real listings.

Buying a repossessed car from a bank or credit union can save you thousands of dollars. One major way they help you save is by offering financing deals as low as 1%. This is something you rarely see at dealerships or auctions. Let’s explore why they do this and how you can benefit.

Banks and credit unions sometimes need to take back cars when people stop making loan payments. These vehicles are called repossessions or “repos.”

When a bank or credit union gets a repo, they don’t want to keep it. They want to sell it quickly and recover their money. The faster they sell, the less they lose.

That’s why they are motivated to offer great financing deals. It helps the vehicle sell faster.

Banks and credit unions are not car dealers. They are lenders. Their goal is to get back their loan balance, not make a profit.

When you buy a repo car directly from a bank or credit union, they may offer you:

These institutions already own the car. So they have room to make the financing attractive.

Repos cost money to hold. Every day a repo sits in a lot, the bank loses more. There are storage costs. There’s depreciation.

Plus, the longer they wait, the harder it becomes to sell. Cars lose value fast. Banks know this.

That’s why they’re willing to cut deals. They’d rather sell fast at a discount than wait and lose more.

Banks and credit unions don’t use high-pressure sales. They are not trying to upsell or hide costs.

This means you have more room to talk about price and terms. Many small banks and local credit unions will work with you.

They may even pre-approve you for financing before you bid on a repo car.

At an auction, you might pay extra fees. You usually have to pay cash. There are no financing deals.

Dealerships mark up their prices. They often add fees for paperwork, delivery, and prep. That adds up fast.

Buying from a bank cuts out the middleman. You get the car at a better price, and you can finance it too.

Many banks and credit unions sell repo vehicles through bidding. Some use sealed bids. Others sell first-come, first-served.

Here’s how it usually works:

Some credit unions will even help arrange transport or offer warranties.

Credit unions are member-owned. That means they care more about people than profit.

They are known for being:

You can expect a personal touch when buying from them. You’ll deal with people, not sales tactics.

Banks and credit unions must follow strict rules. Their repossession sales are legal, fair, and well-documented.

You’ll usually get a clean title. They’ll tell you what they know about the car’s condition.

Many include photos, VIN numbers, and full descriptions. This helps you make an informed decision.

RepoFinder.com is the easiest way to find repo cars from banks and credit unions. It’s free to use and updated often.

Here’s why it’s popular:

You deal directly with the financial institution. That means better deals, honest terms, and more trust.

When buying a repo from a bank, look for:

Ask if they offer rate discounts for automatic payments or being a member.

Here are simple steps to start your search:

Take your time, ask questions, and make sure the deal fits your budget.

Here’s how you can save:

All together, that can mean thousands of dollars in savings.

Let’s say you buy a $15,000 repo car from a credit union with 1% interest over 4 years. Your payments could be around $320/month.

At a dealer, the same car might cost $17,000 with a 6% loan. That’s $398/month. That’s a big difference.

Over 4 years, that’s a savings of more than $3,700.

If you want to save money on your next car, bank repos are a smart move. You’ll get better rates, trusted sellers, and a clear process.

Use RepoFinder.com to start your search. It’s the best place to find bank and credit union repos fast.

Title: How Buying Repo Cars from Banks Saves You Money

+-------------------------------+

| LOW RATES |

| Bank APRs as low as 1% |

+-------------------------------+

| NO DEALER MARKUPS |

| Pay what the bank asks |

+-------------------------------+

| DIRECT FINANCING |

| Apply for a loan on-site |

+-------------------------------+

| TRANSPARENT SALES |

| Photos, VINs, and full info |

+-------------------------------+

| REPOFINDER.COM |

| Nationwide repo listings |

+-------------------------------+